Disclaimer: We provide high-quality, free printable templates to help you organize your personal data. We are not certified financial planners or investment advisors. The tools and information provided below are for educational and organizational purposes only. Always consult a licensed financial professional before making high-stakes decisions regarding investments, asset allocation, tax strategy, or debt consolidation.

A monthly budget works best when it tells your money where to go before the month begins, not after it has already disappeared.

That is exactly why the zero-based budget method is so useful.

Instead of hoping there will be something left at the end of the month for savings, debt payoff, or future goals, this method helps you make those decisions upfront. Every pound or dollar gets a job. Your income comes in, and before the month starts, you decide exactly where it will go.

If you are building a budget binder, a Monthly Budget Planner is one of the most important pages you can include because it gives structure to everything else. It is the page that helps your spending, saving, bill paying, and debt goals all work together.

What is a zero-based budget?

A zero-based budget is a budgeting method where:

Income – Expenses = 0

That does not mean you spend everything carelessly.

It means every bit of income is assigned on purpose.

That includes:

- bills

- groceries

- fuel

- savings

- sinking funds

- debt payments

- personal spending

- anything else you want your money to do

So instead of having “extra money” floating around in your account, you give every amount a clear role.

That is what makes this method so effective. It turns vague money intentions into a real plan.

Why this budgeting method works so well

A lot of people think they are budgeting when they are really just watching what happened after the fact.

They check statements, look at app totals, and try to figure out where things went wrong.

A zero-based budget is different because it is proactive.

It helps you:

- make decisions before spending happens

- reduce “accidental” overspending

- direct extra money toward goals intentionally

- build savings and debt payoff into the month from the start

- feel more in control of your cash flow

That is why this method is so popular. It gives your money structure.

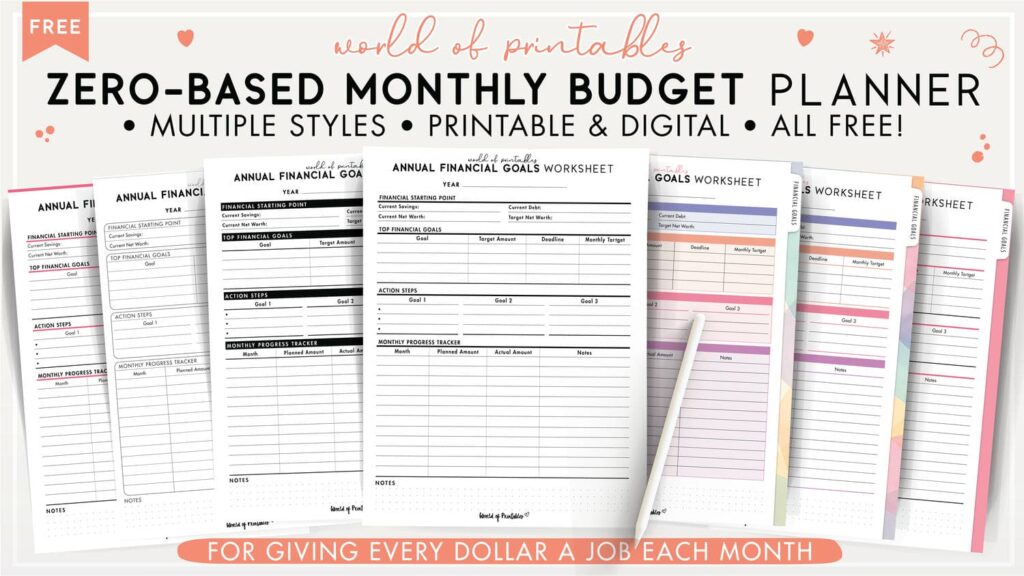

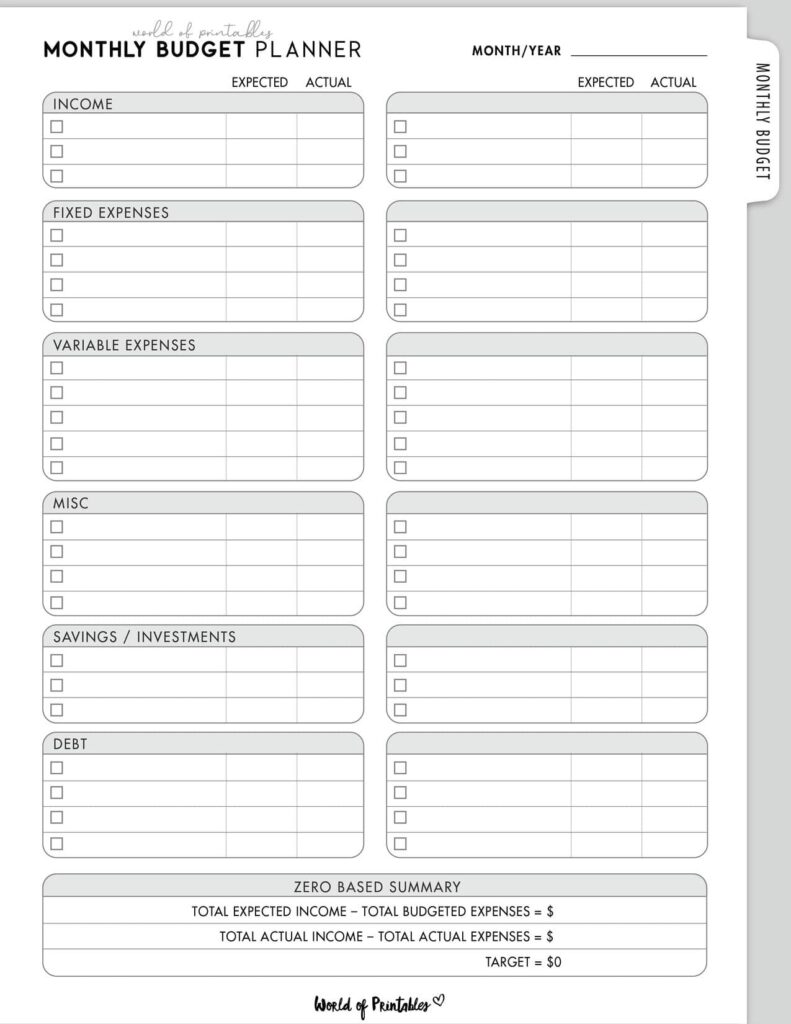

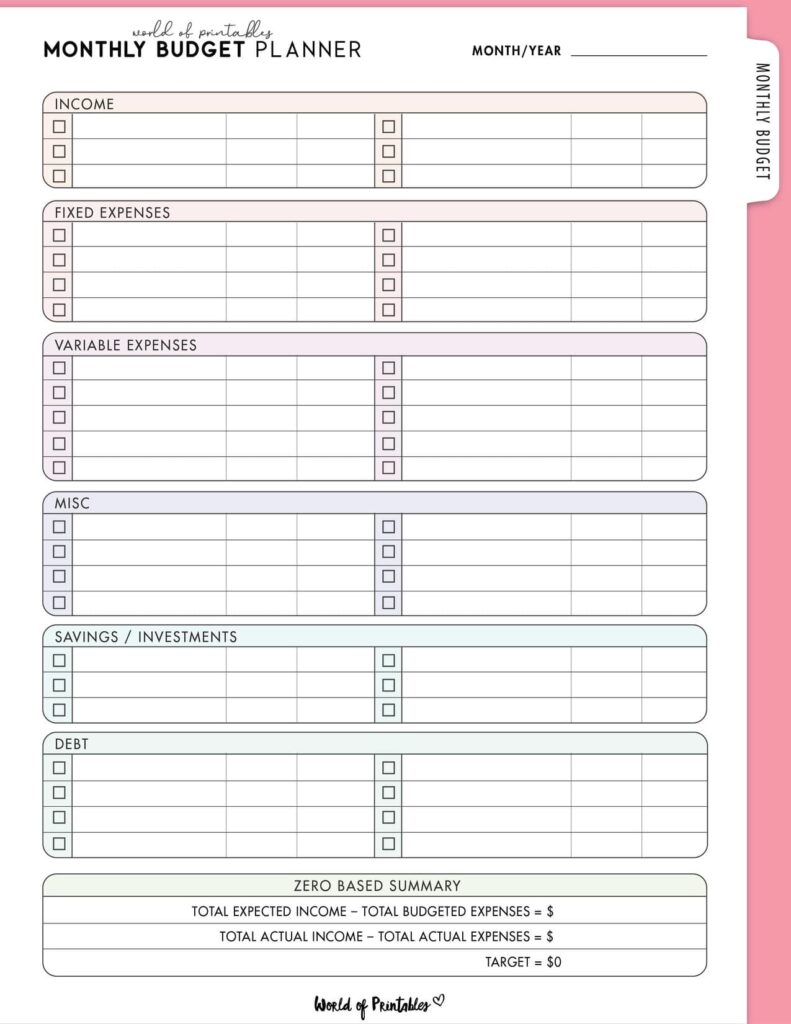

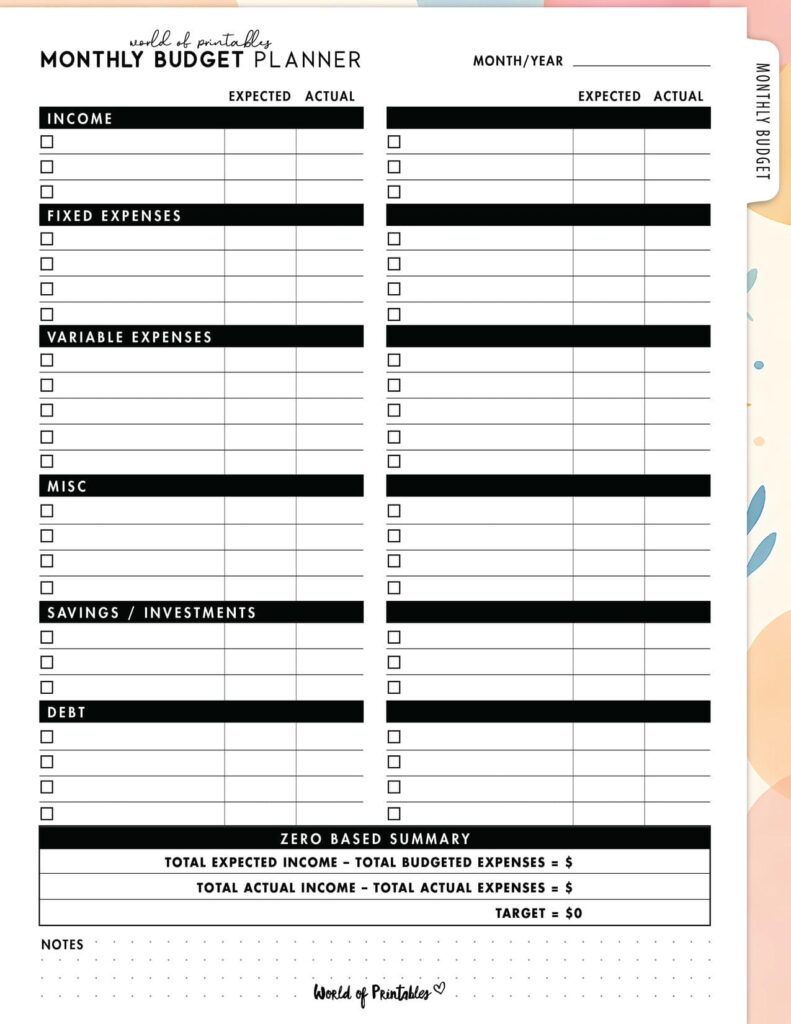

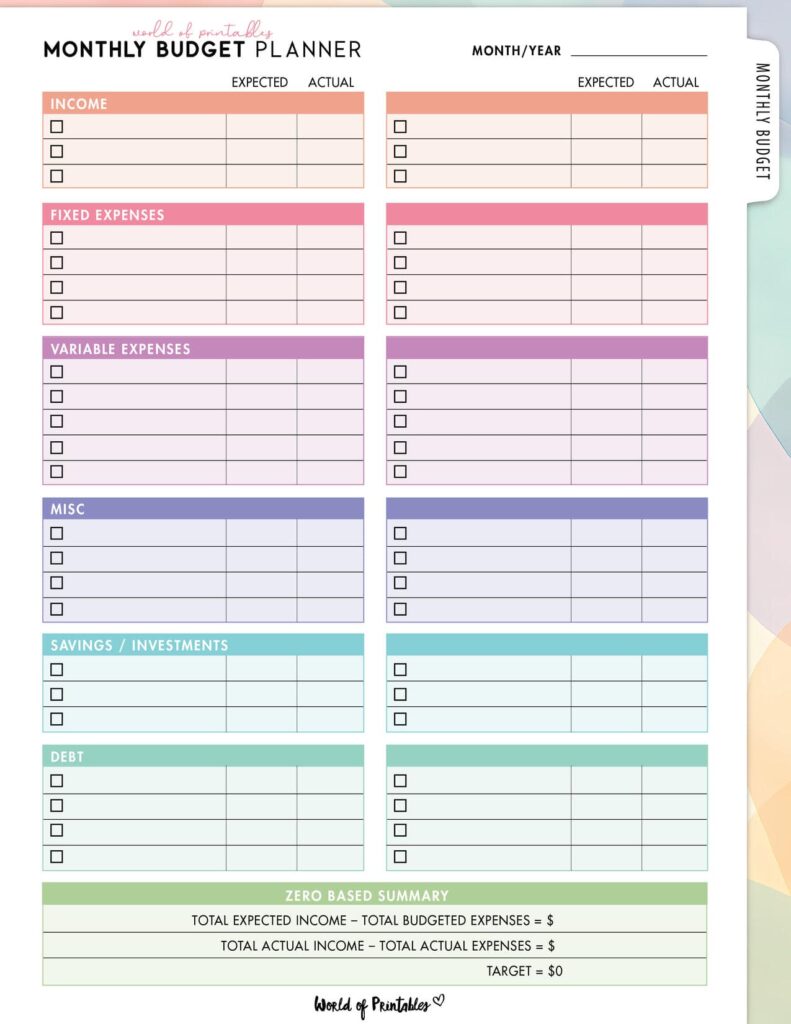

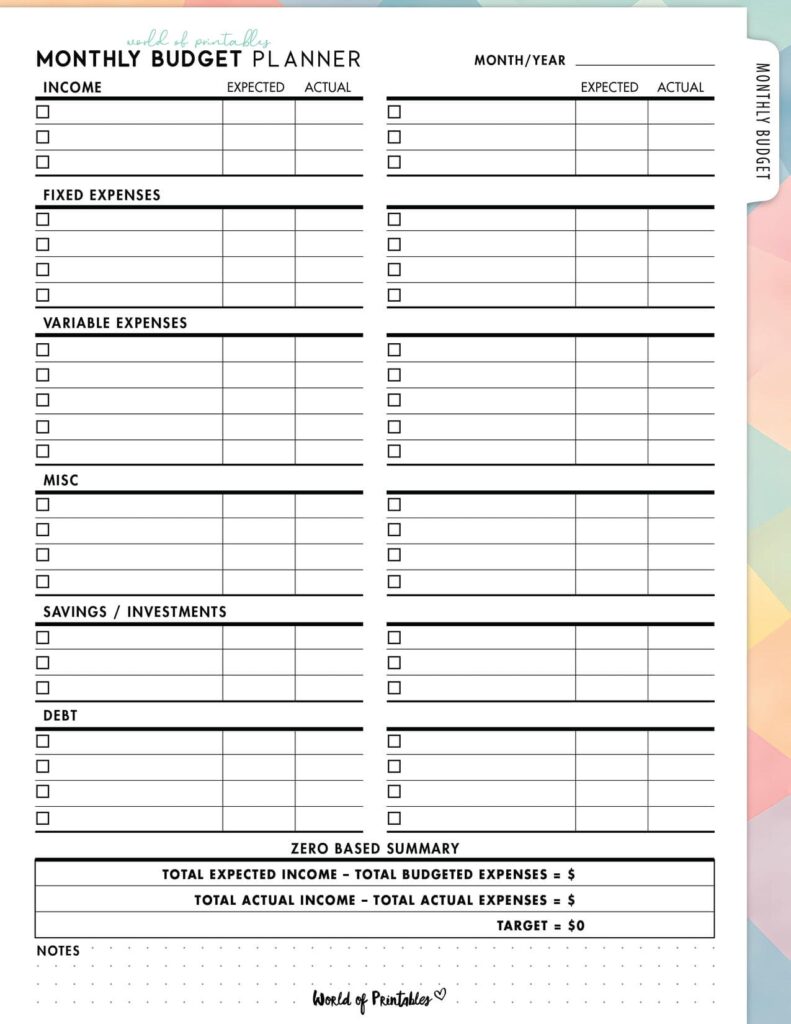

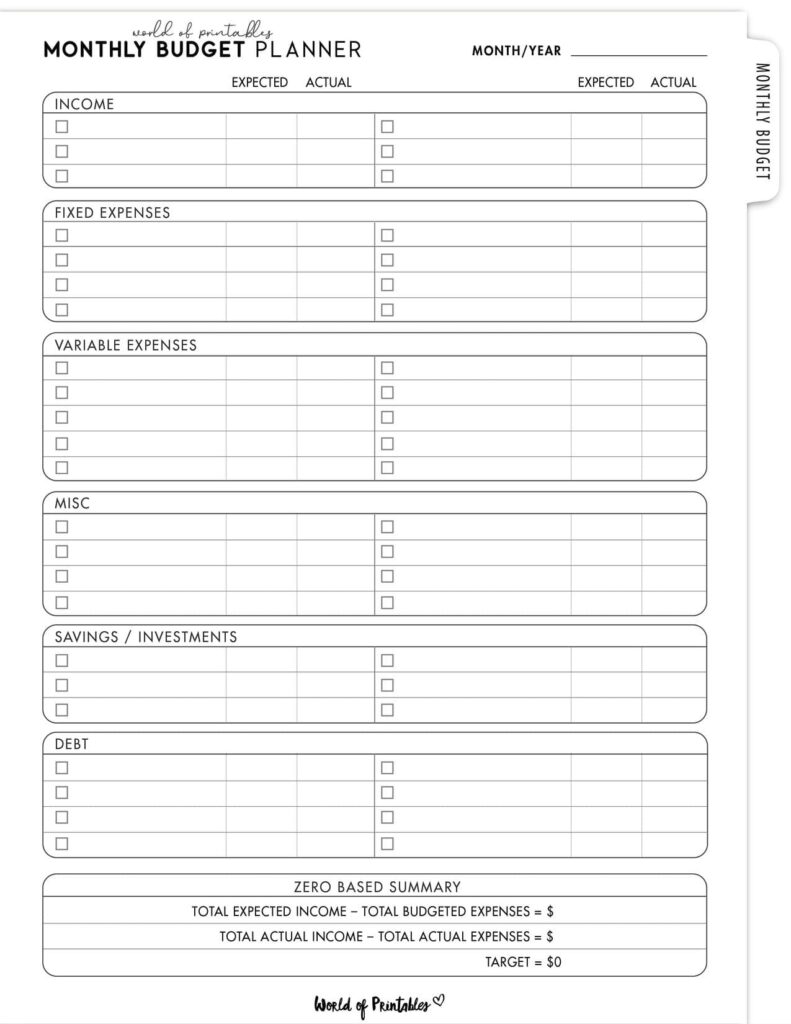

Choose a design theme that fits your style

This printable comes in a range of layouts so you can choose the one that suits your binder and planning style best.

Minimalist and simple styles

These are ideal if you want a clean, distraction-free budget page that keeps the focus entirely on the numbers.

They work especially well in a classic budget binder setup.

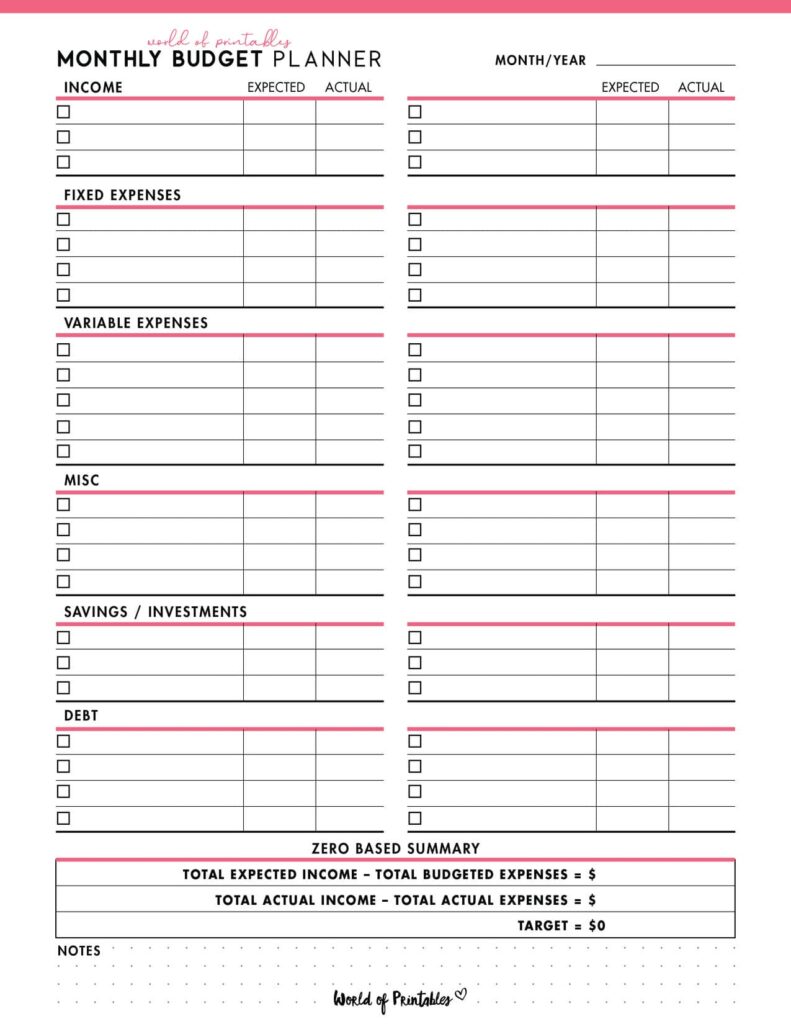

Colorful and visual styles

These are great if you like seeing categories separated clearly at a glance.

That can make it easier to distinguish between income, bills, variable spending, and savings without rereading the whole page.

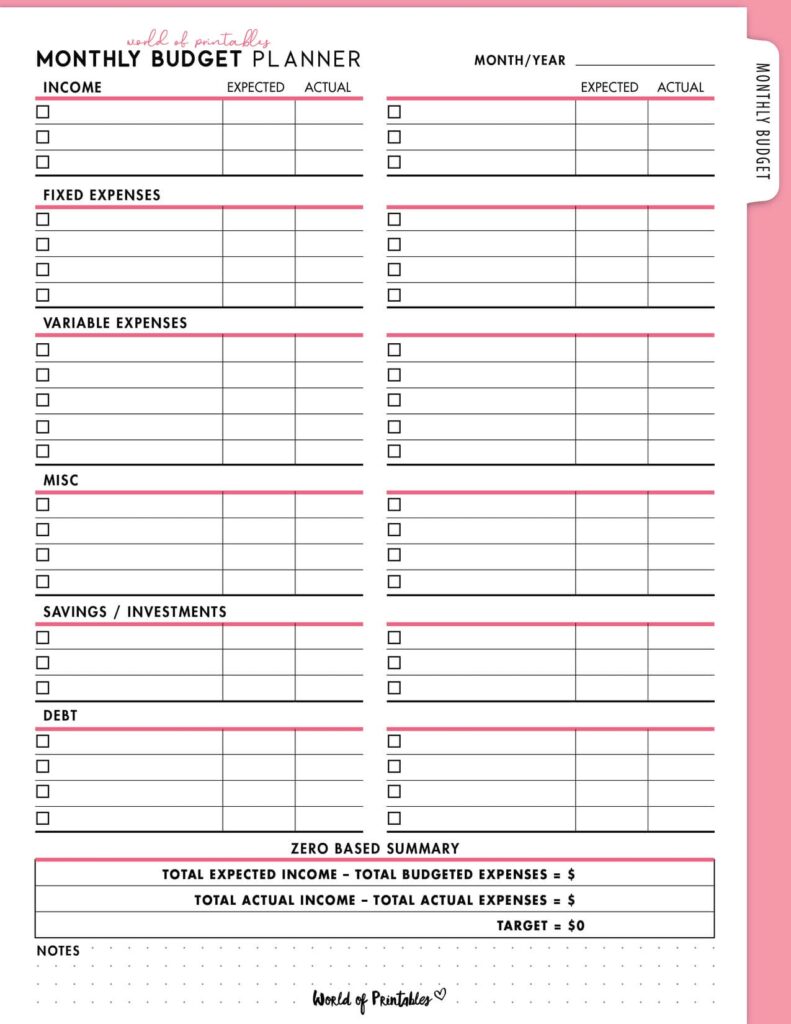

Ink-saving options

If you prefer practical, low-ink printables, these are a smart option.

They still feel polished and organised while being efficient to print month after month.

Free Download and Printing Instructions

To download your free Zero-Based Monthly Budget Planner, click the text link directly beneath the image of your preferred design. This will open the high-resolution PDF.

For the best printing results:

- download the PDF directly to your device

- open the file and select Print

- make sure your printer is set to US Letter

- choose Fit to Page or Scale to Fit so the margins print correctly

If you want this page to hold up well in your binder, it can be worth printing it on slightly thicker paper.

A premium 28 lb or 32 lb paper gives it a more durable, high-quality feel.

Why this printable is so useful in a budget binder

A Monthly Budget Planner is the operational core of a budget binder.

It works especially well alongside:

- bill payment calendars

- daily spending logs

- paycheck budgeting breakdowns

- sinking funds trackers

- debt payoff trackers

- annual financial goals worksheets

Those pages help you manage different parts of your finances.

Your monthly budget planner is what connects them.

It is the page that says:

- this is how much money is coming in

- this is what must be covered

- this is what we are saving for

- this is what is getting paid down

- this is where every remaining pound or dollar is going

That is why it matters so much.

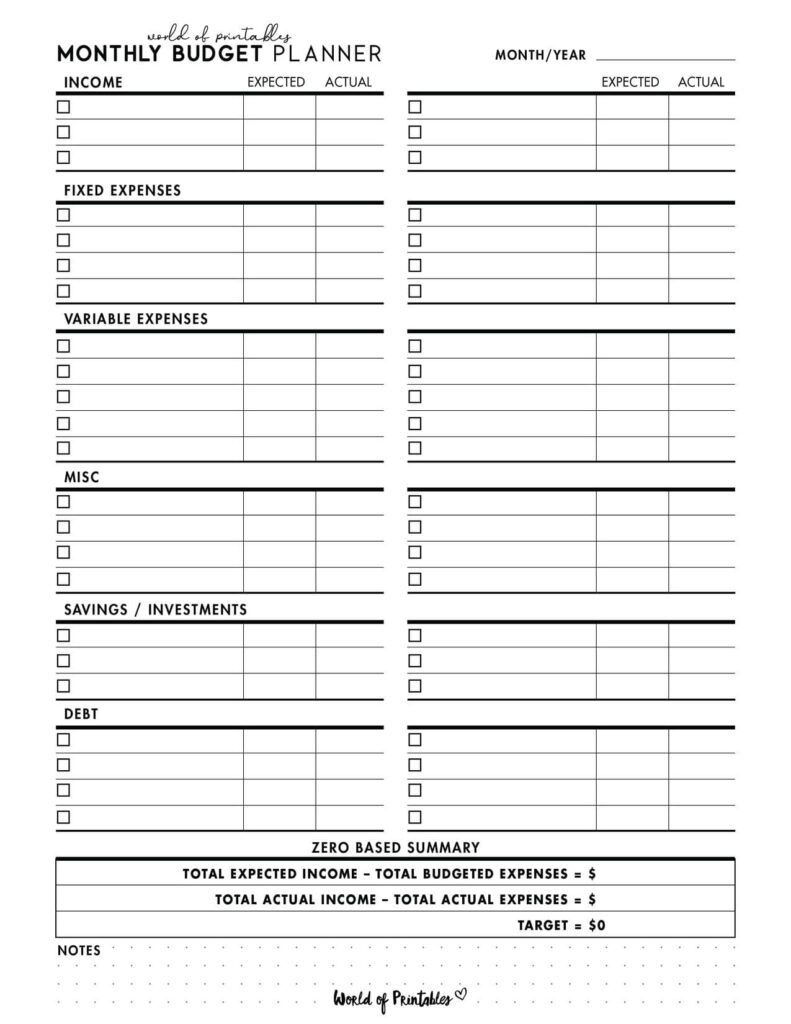

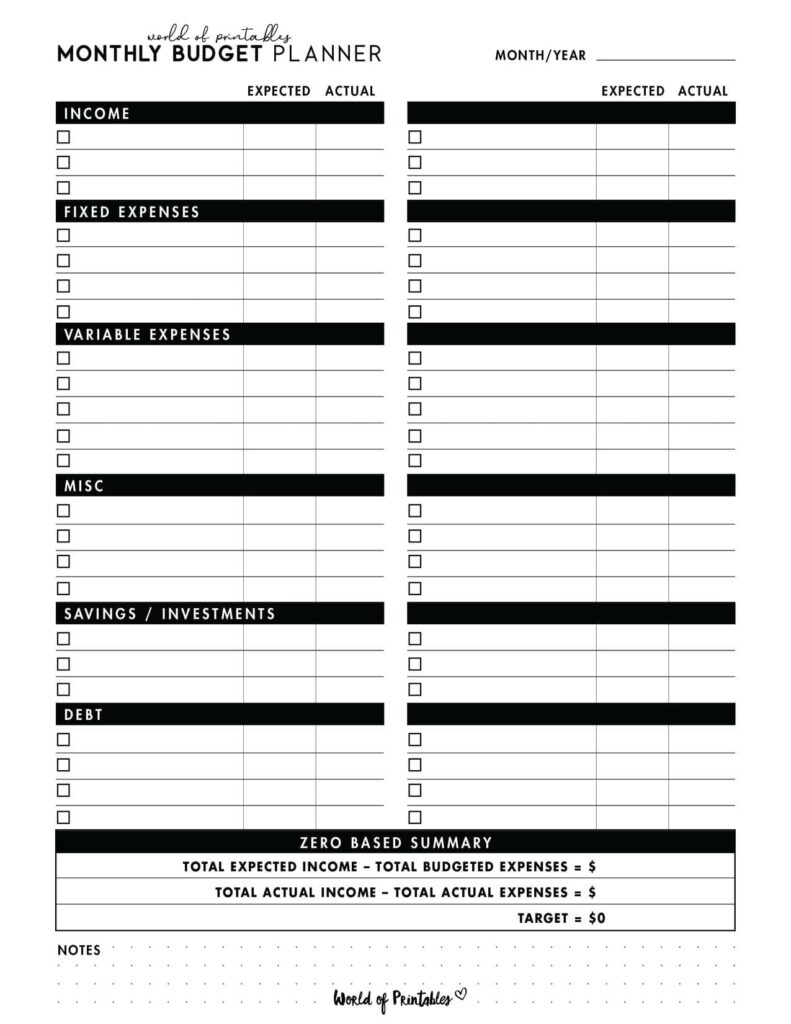

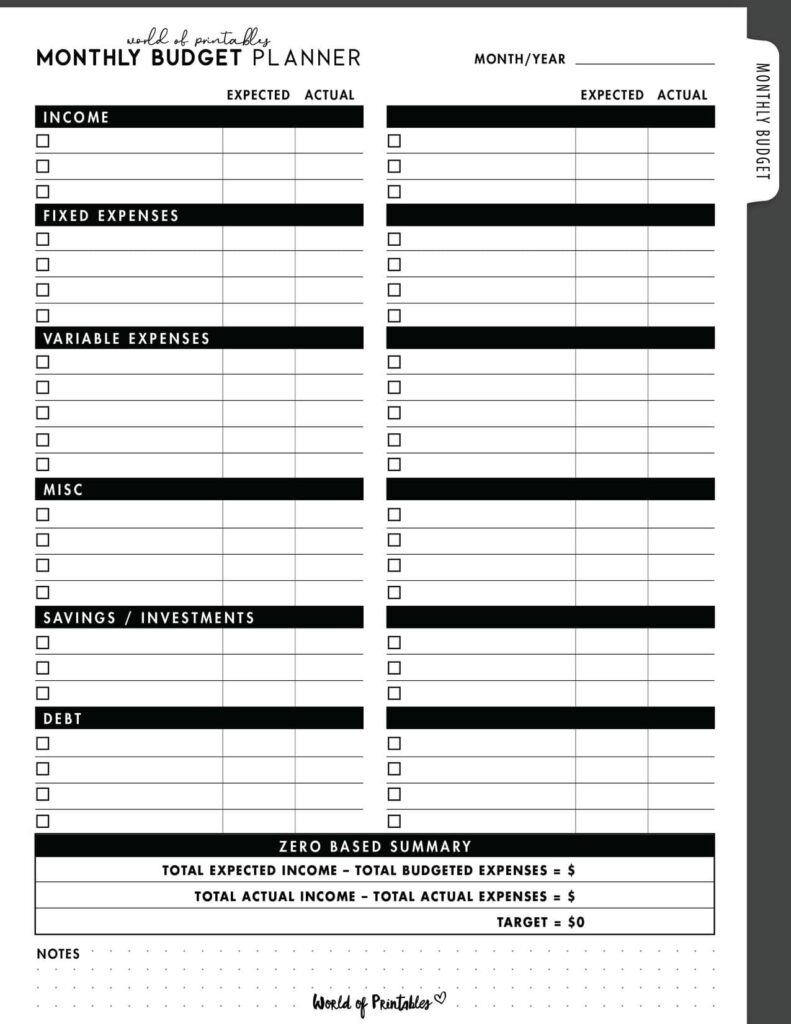

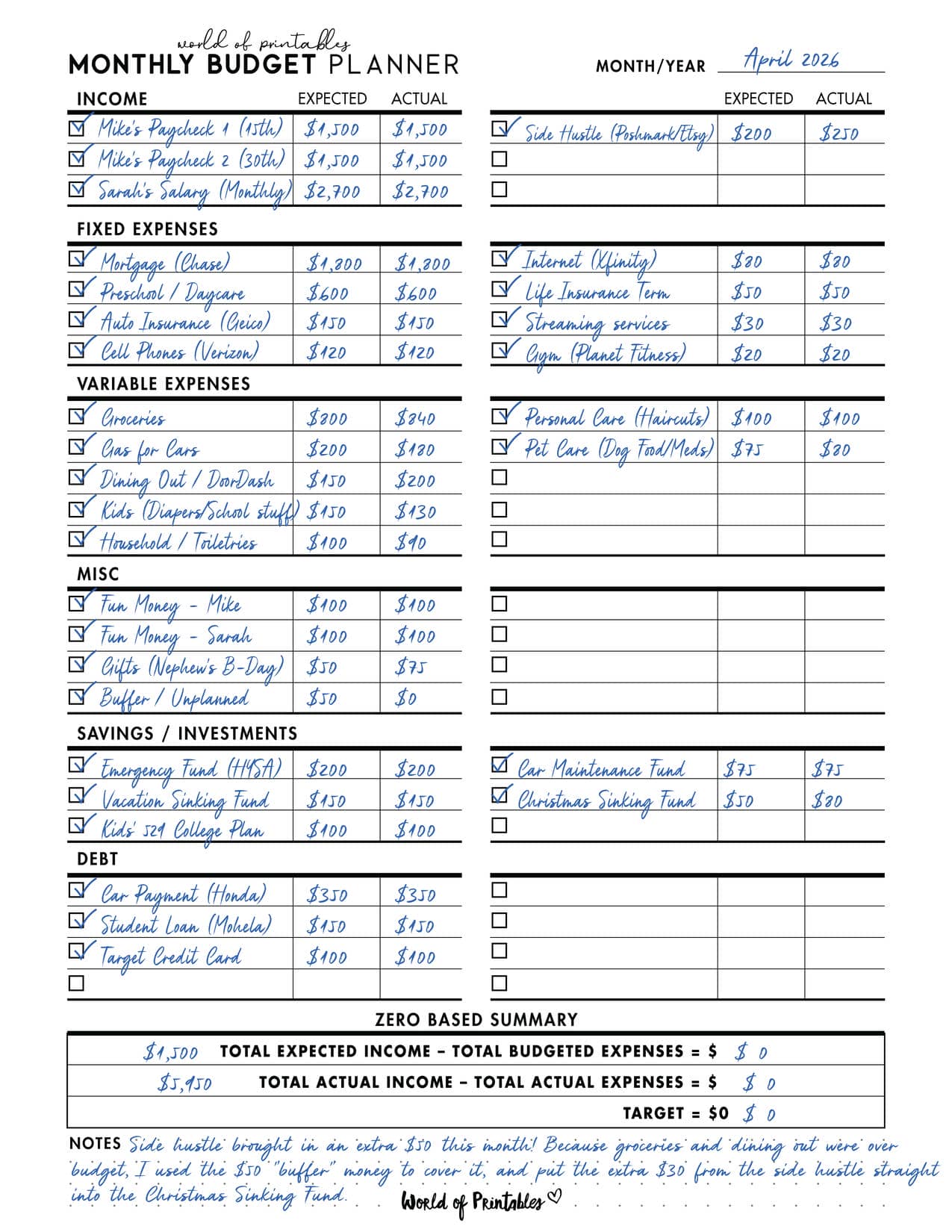

How to Use a Zero-Based Monthly Budget Planner

This is a staple for household management! Zero-based budgeting is incredibly popular right now. The core rule of a zero-based budget is that Total Income minus Total Expenses must equal exactly $0. Every single dollar gets a “job,” even if that job is just going into savings.

Here is a typical example of a filled-in zero-based monthly budget planner:

This printable works best when you fill it out before the month starts.

That way, the plan is already in place before spending begins.

Here is the best way to use it:

Step 1: Write down your total expected income

Start by listing all the income you expect for the upcoming month.

This may include:

- salary or wages

- self-employed income

- side hustle income

- benefits

- support payments

- other regular income

If your income varies, use the most realistic estimate you can based on recent months.

The goal is not to predict perfectly. It is to build the best working plan you can with the information you have.

Step 2: Add your fixed expenses first

Next, list your non-negotiable monthly costs.

These are usually things like:

- rent or mortgage

- council tax

- utilities

- phone and internet

- insurance

- debt minimum payments

- subscriptions you are keeping

- childcare

- transport commitments

These are your foundational costs, so it makes sense to enter them before anything else.

Once they are written down, you can see what your month is already committed to.

Step 3: Estimate your variable spending

Now budget for the categories that can change from month to month.

This often includes:

- groceries

- fuel

- household supplies

- personal spending

- school spending

- entertainment

- dining out

- clothing

- miscellaneous spending

This part works best when you use real data from previous months rather than guessing too optimistically.

A zero-based budget is most useful when it reflects real life, not your fantasy best month.

Step 4: Assign money to savings, debt, and future goals

Now look at what is left after your bills and variable spending.

This is where the zero-based method becomes especially powerful.

Instead of leaving the remainder unplanned, assign it on purpose to things like:

- emergency fund

- sinking funds

- extra debt payments

- holiday savings

- house fund

- investing

- other financial goals

Keep assigning money until your leftover amount reaches zero.

That is the whole point of the method.

Every amount has a job. Nothing is left drifting.

A monthly budget gives you the big picture, but your paydays decide how that plan plays out in real life. Our Paycheck Planner helps you break your monthly budget down into something much easier to use between paychecks.

What categories to include on your monthly budget planner

A useful monthly budget planner should feel complete without becoming overwhelming.

Helpful sections often include:

- total income

- fixed bills

- variable spending

- savings

- debt payments

- sinking funds

- leftover balance

Some people also like to add:

- notes

- financial goals for the month

- a small review section

- expected irregular expenses

The best layout is one that makes it easy for you to see the whole month clearly.

Why “leftover money” often disappears without a plan

One of the biggest strengths of zero-based budgeting is that it removes the illusion of “extra money.”

When money is not assigned, it usually gets absorbed by:

- impulse spending

- casual online shopping

- eating out

- random extras

- spending that feels harmless in the moment

That is why zero-based budgeting can feel so effective so quickly.

It closes that gap.

Instead of wondering where the leftover money went, you already told it where to go.

A realistic note: your budget does not have to be perfect

A budget is a plan, not a prediction machine.

Some months will not go exactly to plan. That is normal.

The goal of a zero-based budget is not to create a flawless month. It is to create a much better starting point.

Even when adjustments are needed, you are still working from a plan instead of reacting to chaos.

That alone makes a big difference.

Who this printable is especially helpful for

This page is a great fit if you:

- want a clearer monthly money plan

- feel like your money disappears too easily

- are trying to save or pay off debt more intentionally

- like structured financial planning

- want your budget binder to feel useful and connected

- prefer proactive budgeting over reviewing spending after the damage is done

It is especially helpful if you often reach the middle or end of the month wondering where the money went.

A simple tip that makes zero-based budgeting easier

If the full month feels too broad, pair this printable with a paycheck budgeting breakdown or daily spending log.

That way:

- the monthly budget gives you the big picture

- the paycheck page handles timing

- the spending log helps you stay on track mid-month

Those pages work beautifully together.

A good question to ask before you finish your budget

Ask yourself:

Have I told every pound or dollar what to do?

If the answer is no, keep going.

That final leftover amount is where a lot of good intentions quietly disappear.

Give it a job before the month starts.

Next Step: Build Your Complete Financial Command Binder

A zero-based budget helps you plan your month with much more intention, but it works even better when it is supported by the right tracking pages.

Helpful pages to add next include:

- a daily spending log

- a paycheck budgeting breakdown

- a bill payment calendar

- a sinking funds tracker

- an annual financial goals worksheet

A zero-based budget tells your money where to go, but you still need to verify that it actually went there.

Together, these pages help you not only create a better plan for your money, but also follow it much more confidently throughout the month.

Complete your monthly cash flow system by adding the next essential tracking tools to your binder:

- Return to the Ultimate Budget Binder Index.

- Download the Daily Spending Log to diagnose cash leaks and keep your zero-based budget on track mid-month.

- Get paid bi-weekly? Download the Paycheck Budgeting Breakdown to map specific bills to specific pay periods.

More budgeting templates

You’ll find many more budgeting templates right here on World of Printables.

AI TRANSPARENCY: Whilst the majority of our creations have been created completely traditionally, occasionally we utilize AI tools in our design process. We acknowledge the advancements in AI technology and leverage them responsibly to optimize our creative output. However, it is important to note that our utilization of AI does not compromise the human element of our work. Our commitment to delivering high-quality designs through a balanced integration of traditional expertise and AI enhancements remains paramount.