Disclaimer: We provide high-quality, free printable templates to help you organize your personal data. We are not certified financial planners or investment advisors. The tools and information provided below are for educational and organizational purposes only. Always consult a licensed financial professional before making high-stakes decisions regarding investments, asset allocation, tax strategy, or debt consolidation.

If your money currently lives in five different places, you are not alone.

Maybe your bills are in your email, your spending is all over your bank app, your savings goals are floating around in your head, and your debt payoff plan changes every time you feel stressed. It is hard to feel in control of your finances when everything feels scattered.

That is exactly why this Budget Binder exists.

This is not just a collection of random budget sheets. It is a complete printable system designed to help you organize your money in one place, stay on top of your bills, track your spending, pay off debt, build savings, and finally feel like you know what is going on with your finances.

Inside this Budget Binder collection, you will find printables for:

- monthly budgeting

- bill tracking

- paycheck planning

- daily spending logs

- debt payoff

- sinking funds

- savings challenges

- credit tracking

- tax prep

- account organization

- and bigger-picture money planning too

Whether you are trying to stop living paycheck to paycheck, get ahead of your bills, pay off credit cards, save for future expenses, or simply feel less anxious every time you open your banking app, these printables help you create a system that works in real life.

Every printable is available in 10+ design themes, including minimalist and simple styles, colorful and visual layouts, and ink-saving options, so you can build a binder that feels both useful and personal.

Want a more hands-on way to use your budgeting pages day to day? Our Paycheck Planner helps you plan around real paydays, map bills to each paycheck, track spending between pay periods, and review what changed before the month ends.

Below, you will find the full Budget Binder library, organized by category so you can pick the pages that fit your life best and build your own system step by step.

Why a physical budget binder can work so well

Digital tools are useful, of course. But there is something very different about sitting down with your numbers on paper.

A physical binder helps because it:

- keeps everything in one place

- makes your finances easier to review at a glance

- reduces the mental clutter of jumping between apps and accounts

- gives you a routine for checking in with your money

- helps you move from “I think I’m doing okay” to “I can see exactly what’s happening”

A binder also makes it easier to connect the dots.

Your monthly budget is no longer separate from your debt plan. Your savings challenge is no longer floating around without context. Your bill calendar, sinking funds, net worth tracker, and spending logs all support each other.

That is what makes this kind of system so powerful.

What this binder helps you do

A well-built budget binder helps you do much more than just “track spending.”

It helps you:

- Get clear on your cash flow

Know what is coming in, what is going out, and where your money needs to go next. - Stay ahead of bills

See due dates, plan around paydays, and reduce the stress of forgotten payments. - Pay off debt with purpose

Use structured methods like the debt snowball or debt avalanche instead of throwing random extra payments around. - Build savings intentionally

Create sinking funds, emergency savings, and weekly challenge plans that actually fit your life. - Review the bigger picture

Track your net worth, annual goals, and year-end progress so you can see whether your overall strategy is working. - Stay organised for tax time

Keep medical expenses, charitable donations, and other records together throughout the year. - Store key information in one place

Create a secure reference section for important account details and financial admin pages.

How this budget binder is organised

To make the system practical and easy to build, the printables are organised into clear sections.

You do not need to use every single page straight away. Start with the sections that solve your biggest current problems, then expand as needed.

Phase 1: High-Level Financial Planning

This section is about the bigger picture. It helps you zoom out and look at where your finances are going overall, not just what is happening this week.

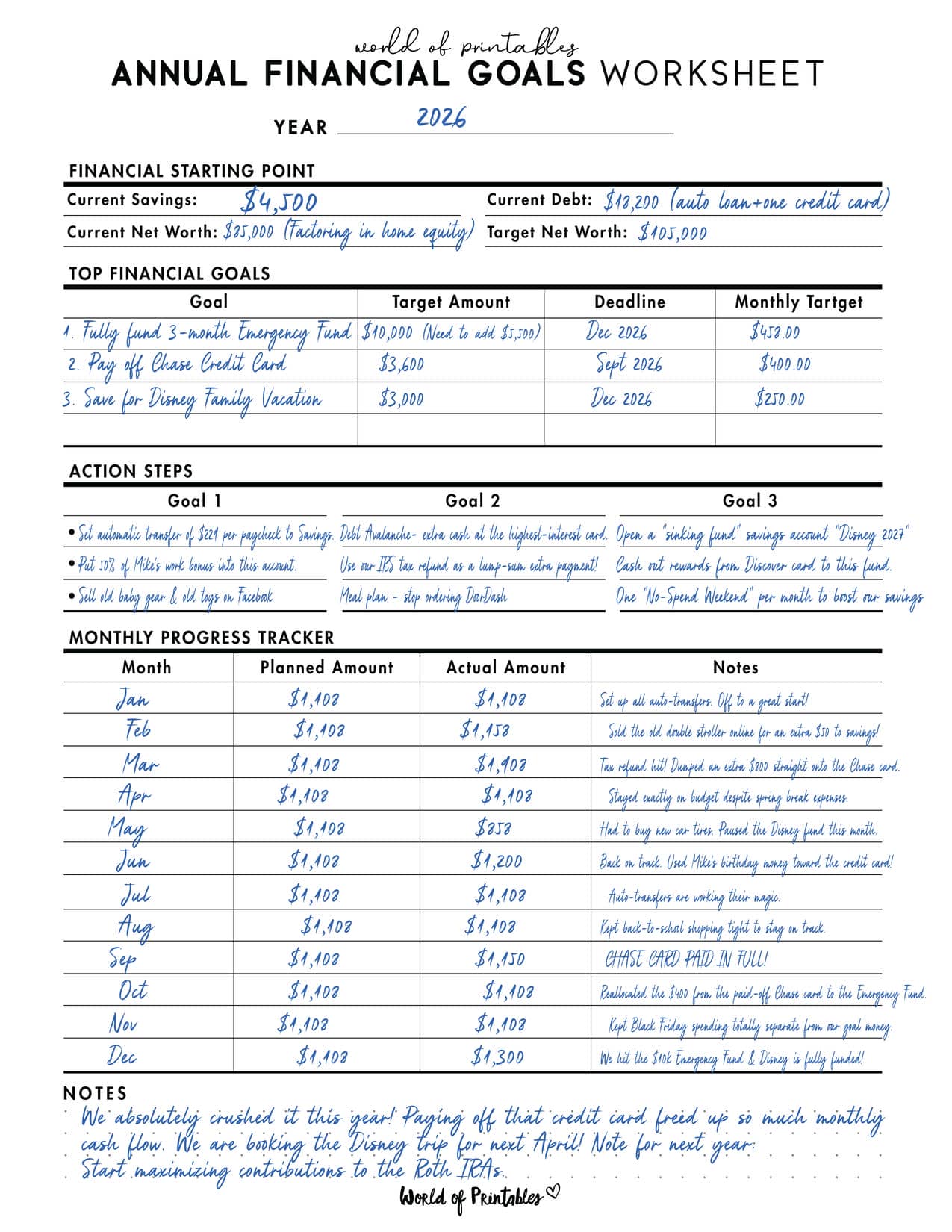

1. Annual Financial Goals Worksheet

Start here if you want to set financial priorities for the year ahead.

This worksheet helps you define:

- short-term goals

- medium-term goals

- long-term goals

- monthly targets that support those goals

The problem:

You work hard, make decent money, and still end every year wondering why you are not closer to the things that really matter, like a house down payment, a full emergency fund, a paid-off credit card, or a family vacation you can actually afford.

What it is:

A one-page planning sheet for mapping out your short-term, medium-term, and long-term financial goals.

What it’s really good for:

Turning vague hopes into a real plan. This is the page that helps you stop saying, “I hope we can do that someday,” and start saying, “We need to save $300 a month to make that happen.” It gives your money direction before the year slips away again.

This section is about the bigger picture. It helps you zoom out and look at where your finances are going overall, not just what is happening this week.

Click here to get the free Annual Financial Goals Worksheet.

2. Net Worth Tracker

This is one of the most important “big picture” pages in the binder.

It helps you track:

- what you own

- what you owe

- how your overall financial position changes over time

The problem:

You open your banking app, see a low checking balance, and immediately feel like you are getting nowhere. Meanwhile, you may be paying down debt, building home equity, growing retirement savings, or increasing your total assets without even noticing the bigger progress.

What it is:

A simple tracker that compares everything you own with everything you owe.

What it’s really good for:

Showing you the bigger picture. Instead of measuring your financial life by whatever happens to be sitting in checking that day, you get a much more honest view of your overall progress. It is one of the most motivating pages in the binder because it helps you see that your efforts are actually adding up.

Click here to get the free Net Worth Tracker.

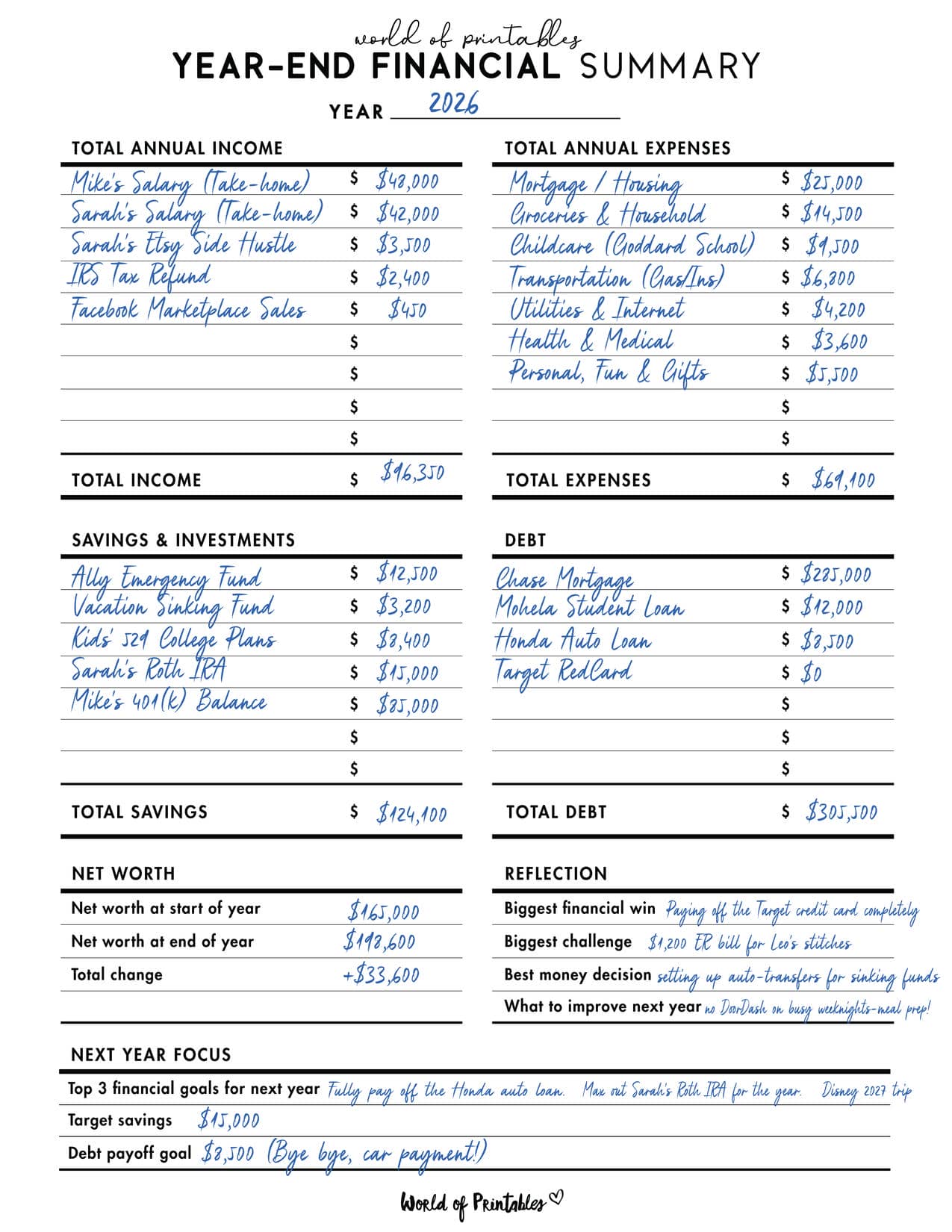

3. Year-End Financial Summary

Use this to review the full year in one place.

It helps you total:

- annual income

- annual expenses

- savings progress

- debt reduction

- financial lessons and trends

The problem:

You get to the end of the year, look at your total income, and wonder how you earned that much and still feel like the money vanished.

What it is:

A one-page annual review of your income, spending, savings, and debt payoff.

What it’s really good for:

Giving you the truth in one place. This page helps you see what really happened over the past 12 months, what categories quietly drained your money, how much progress you actually made, and what needs to change before the new year starts. It is the kind of reality check that can completely reset the way you budget going forward.

Click here to get the free Year-End Financial Summary.

Bonus Printable: Retirement Tracker Template

This page helps you keep long-term saving visible, especially if retirement contributions are part of your bigger wealth plan.

Click here to get the free Retirement Tracker Template.

Phase 2: Cash Flow and Budgeting

This section is the working core of your monthly money system.

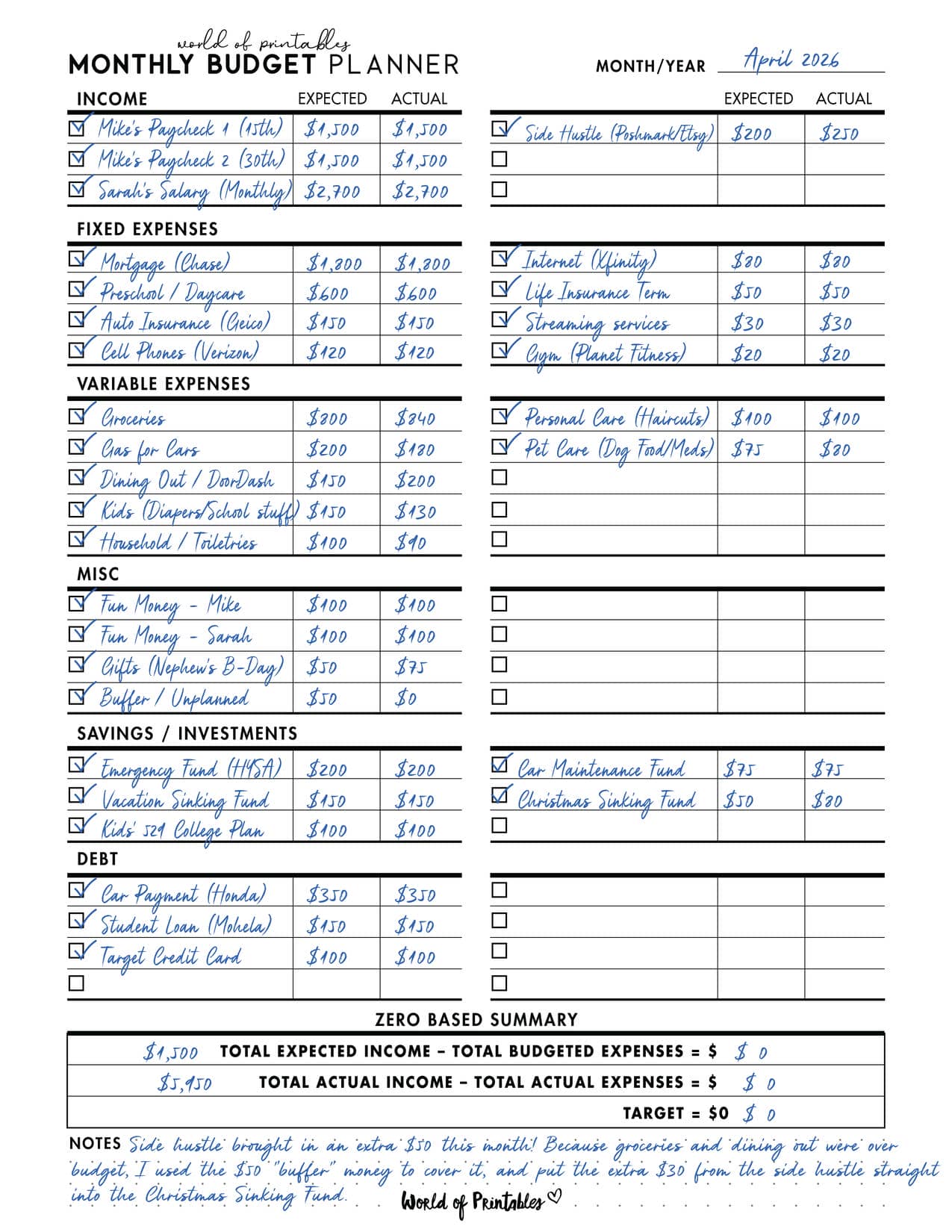

4. Monthly Budget Planner (Zero-Based)

This is your main monthly planning page.

It helps you:

- assign every pound or dollar a job

- plan bills, spending, savings, and debt payments

- reduce the “where did it all go?” feeling

The problem:

Your paycheck lands, bills start coming out, you swipe for groceries and gas, and then you spend the rest of the month hoping everything else will somehow still get covered.

What it is:

A monthly planner built around the zero-based method, where every single dollar gets assigned a job before the month begins.

What it’s really good for:

Replacing money stress with clarity. Instead of wondering whether you can afford something, you already know. Every dollar has a purpose, whether that is the power bill, groceries, debt payoff, savings, or fun money. It is one of the best ways to stop feeling like your money disappears on you.

Click here to get the free Monthly Budget Planner (Zero-Based).

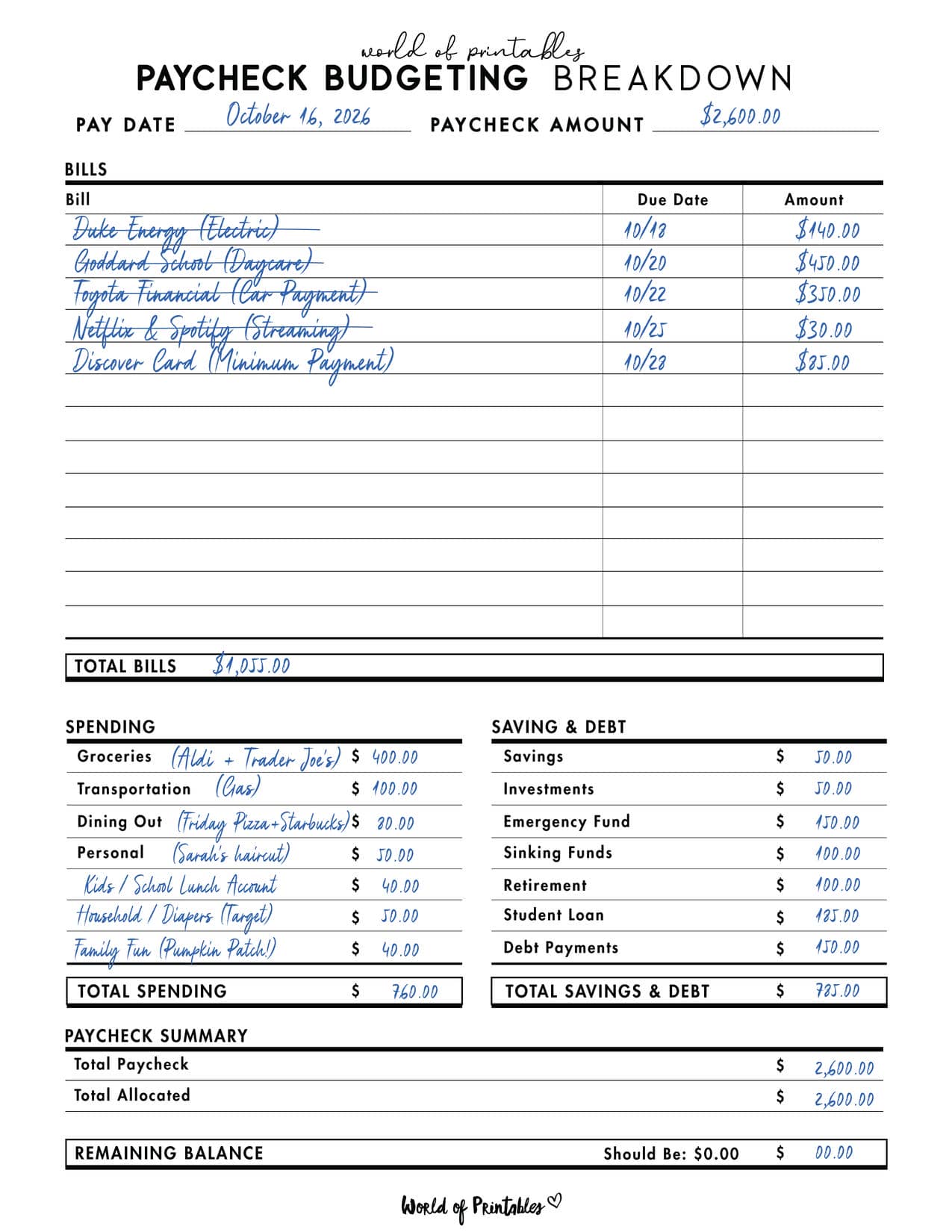

5. Paycheck Budgeting Breakdown

Perfect if you are paid bi-weekly, weekly, or semi-monthly.

This page helps you:

- split your monthly plan into real-life pay periods

- map bills to the correct paycheck

- reduce mid-month money stress

The problem:

Your monthly budget looks fine on paper, but real life does not line up so neatly. Bills are due early, paychecks arrive later, and you are constantly doing mental math trying not to overdraft.

What it is:

A worksheet that breaks your monthly budget into smaller pay-period plans.

What it’s really good for:

Making your actual cash flow make sense. If you are paid bi-weekly, weekly, or twice a month, this page helps you map specific bills and spending to specific paychecks so you know exactly what each one needs to cover. It is a huge help for reducing that constant “can I safely spend this right now?” anxiety.

Click here to get the free Paycheck Budgeting Breakdown.

Bonus Printable: Envelope Budgeting System

A great option if you like assigning fixed amounts to categories and working with more visible spending boundaries.

Click here to get the free Envelope Budgeting System.

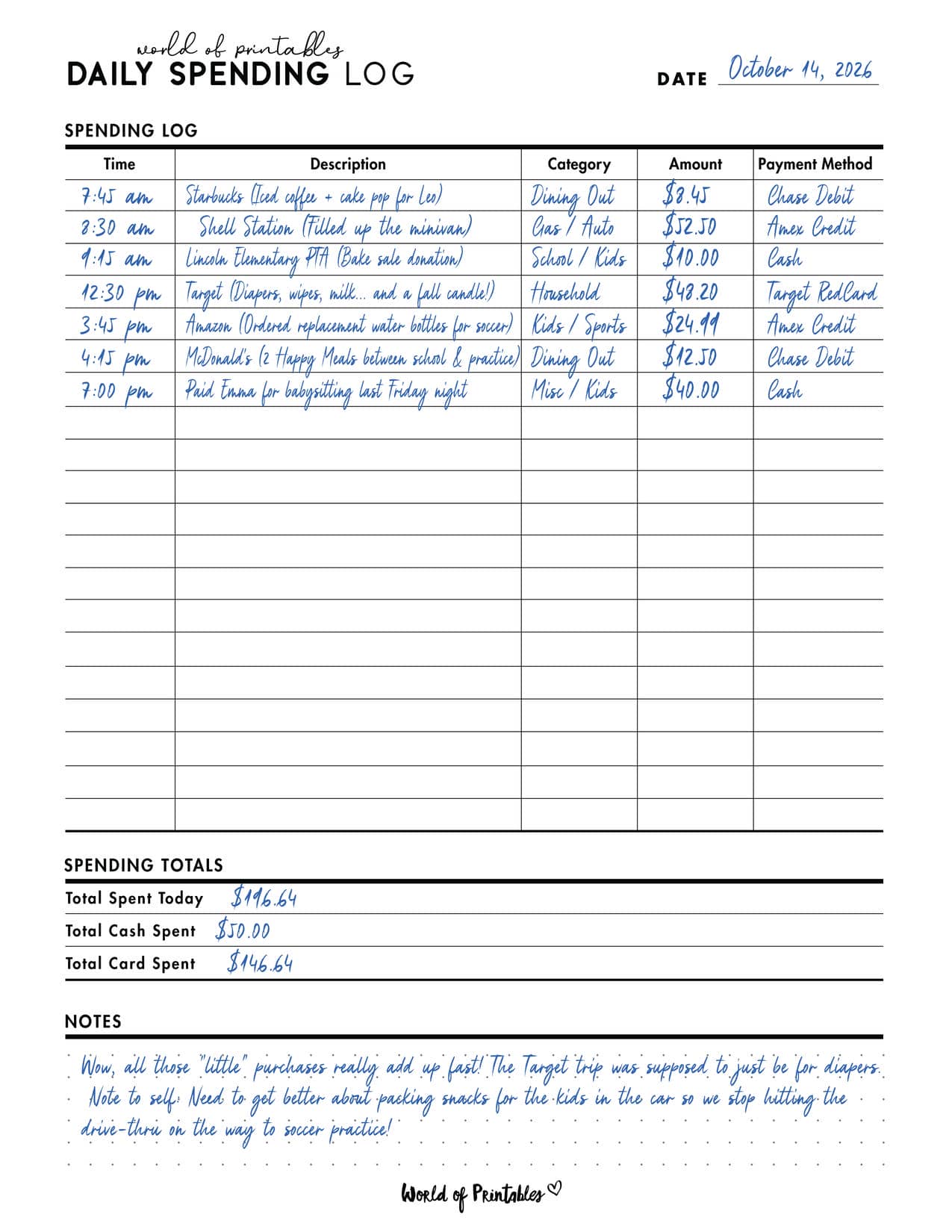

6. Daily Spending Log

This page helps you track the reality of your spending during the month.

It is especially useful for:

- catching leaks early

- spotting impulse spending

- staying aligned with your budget

The problem:

Most budgets do not get wrecked by one giant purchase. They get chipped away by all the small, forgettable spending. The coffee, the Target extras, the quick drive-thru stop, the random Amazon order that did not feel like much at the time.

What it is:

A simple daily spending sheet where you record purchases as they happen.

What it’s really good for:

Creating a pause before spending becomes automatic. The moment you know you have to write the purchase down, it feels more real. That little bit of friction can stop a surprising number of impulse buys and help you catch the quiet leaks in your budget before they get out of hand.

Click here to get the free Daily Spending Log.

Phase 3: Debt Destruction

If debt payoff is a priority, this section helps you build a clear strategy rather than relying on good intentions.

7. Debt Snowball Tracker

Best for motivation and fast emotional wins.

You pay off:

- the smallest balance first

- then roll the payment into the next one

The problem:

When you have multiple debts, making minimum payments on everything can feel like shouting into the void. You pay and pay, but nothing seems to disappear, which makes it easy to lose hope fast.

What it is:

A visual debt payoff tracker based on the debt snowball method, where you start with the smallest balance first.

What it’s really good for:

Building momentum quickly. Paying off one smaller debt completely gives you a real win early on, and that win matters. It helps debt feel beatable. You clear one account, roll that payment into the next, and start creating the kind of progress that keeps you going.

Click here to get the free Debt Snowball Tracker.

8. Debt Avalanche Tracker

Best for efficiency and interest savings.

You pay off:

- the highest interest rate first

- then move down the list mathematically

You do not need both at once. Choose the one that fits your personality and the kind of momentum you need.

The problem:

If your debts have high interest rates, a big chunk of every payment can disappear into interest before it even touches the balance. That can make payoff feel painfully slow.

What it is:

A debt payoff tracker based on the avalanche method, where you target the highest interest rate first.

What it’s really good for:

Saving money and speeding up your payoff plan. This method is ideal if you want the most efficient route out of debt. By attacking the balance costing you the most in interest, you reduce what you lose over time and make your extra payments work much harder.

Click here to get the free Debt Avalanche Tracker.

Phase 4: Bill Management and Solvency

This section helps you stay ahead of recurring obligations and keep your financial admin under control.

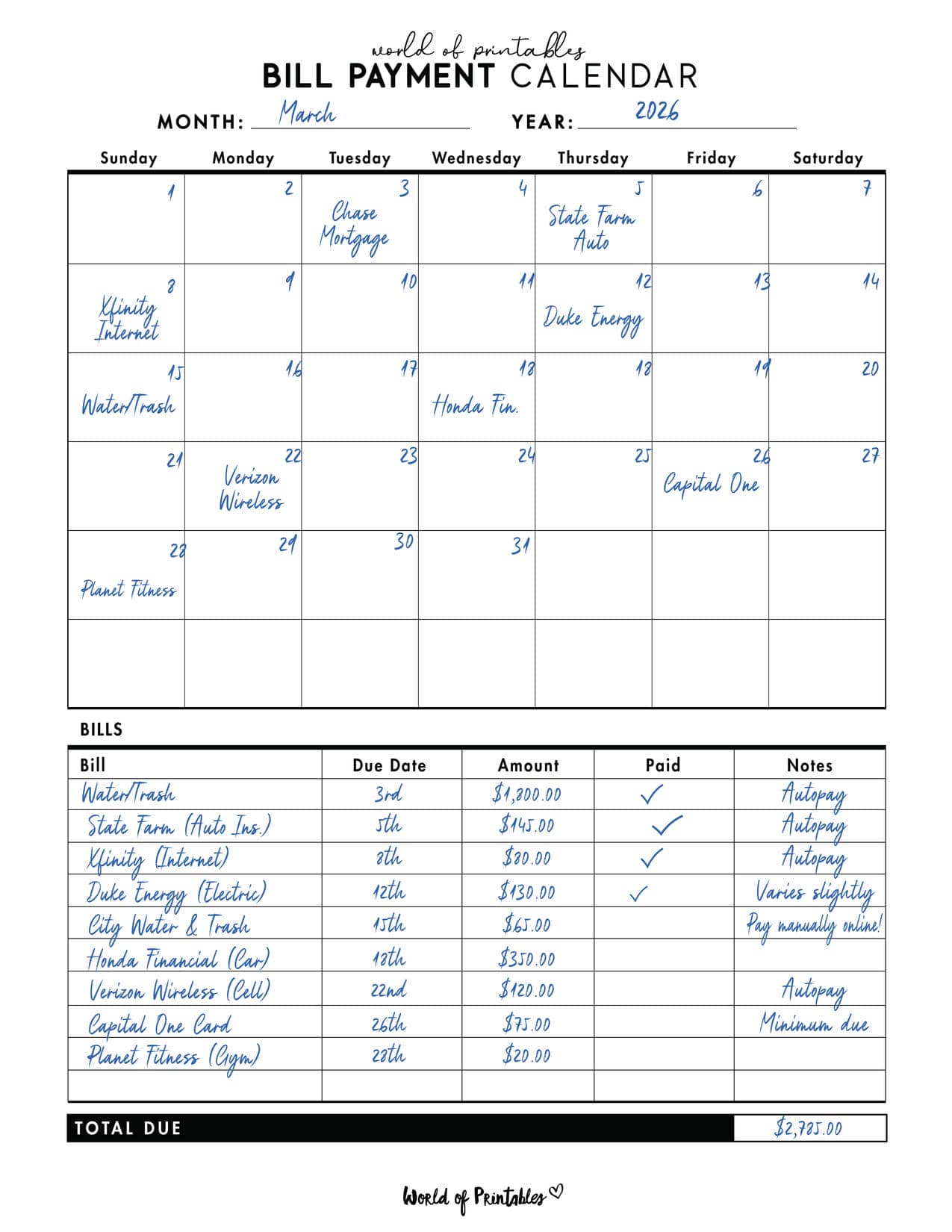

9. Bill Payment Calendar

A monthly visual overview of your bill due dates.

This helps you:

- see what is due and when

- track what has cleared

- reduce late payment stress

The problem:

Sometimes it is not that you do not have the money. It is that you forgot the due date, lost track of what cleared, or assumed a payment was handled when it was not. That is how late fees and avoidable stress show up.

What it is:

A monthly calendar dedicated to bill due dates and payment tracking.

What it’s really good for:

Giving you peace of mind. This is the page that lets you see your month clearly, know what has been paid, and stop second-guessing yourself. When your bills are mapped out in one place, it becomes much easier to stay ahead of them.

Click here to get the free Bill Payment Calendar.

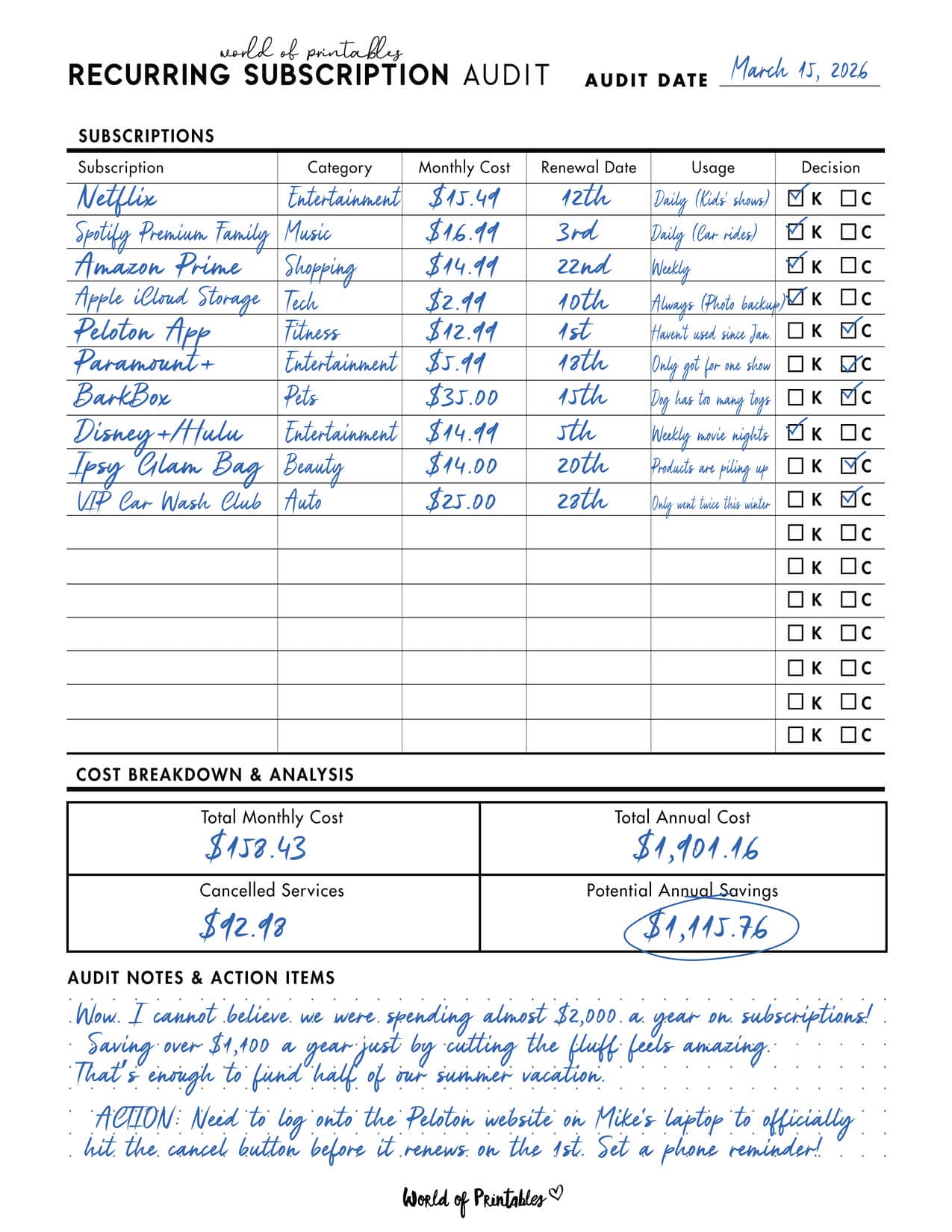

10. Recurring Subscription Audit

Use this to review and cut the charges that have quietly become part of your monthly spending.

This page is great for:

- streaming services

- apps

- memberships

- recurring deliveries

- forgotten auto-renewals

The problem:

A few forgotten subscriptions can quietly drain your budget month after month. Streaming services, apps, memberships, auto-renewals, little charges that feel harmless until you add them all up.

What it is:

A simple audit page for reviewing all of your recurring subscription payments.

What it’s really good for:

Finding money fast. This is one of the easiest ways to free up room in your budget without touching essentials. A quick audit can reveal charges you barely use and no longer need, which often feels like giving yourself an instant raise.

Click here to get the free Recurring Subscription Audit.

11. Credit Score Tracker

A simple way to monitor your score over time and keep your credit health visible.

The problem:

You assume your credit is fine until the exact moment you need it, then find out your score dropped because of a missed bill, an error, or something much more serious like fraudulent activity.

What it is:

A monthly tracker for recording your credit score, limits, and any major changes.

What it’s really good for:

Helping you catch problems before they matter. When you track your score regularly, you are much more likely to notice sudden drops, spot possible errors, and understand what is affecting your credit before you apply for something important.

Click here to get the free Credit Score Tracker.

Phase 5: Targeted Savings and Sinking Funds

This section helps you prepare for both planned costs and future goals.

12. Sinking Funds Tracker

One of the most practical pages in the whole binder.

Use it to save gradually for:

- Christmas

- birthdays

- car maintenance

- annual bills

- holidays

- school costs

- home expenses

The problem:

The same expensive seasons and annual costs show up every year, and somehow they still end up feeling like emergencies. Christmas, school shopping, insurance renewals, car repairs, birthdays, holidays. None of it is random.

What it is:

A tracker for saving gradually toward known future expenses.

What it’s really good for:

Helping you handle predictable costs without panic. Instead of scrambling or swiping a credit card when those bills arrive, you save small amounts ahead of time and pay cash when the time comes. It is one of the best tools for smoothing out your budget all year long.

Click here to get the free Sinking Funds Tracker.

Bonus Printable: Emergency Fund Tracker

This helps you build a proper safety net for real emergencies, separate from your sinking funds.

Click here to get the free Emergency Fund Tracker.

13. No-Spend Challenge Tracker

A great reset page for months when spending has drifted and you want to rebuild discipline and free up cash quickly.

The problem:

Sometimes spending gets so automatic that you look at your bank balance and genuinely do not know how you spent that much in such a short time.

What it is:

A visual challenge tracker for pausing non-essential spending for a set number of days.

What it’s really good for:

Giving your habits a reset. This page turns a spending freeze into something visible and motivating. It helps you break the cycle of mindless purchases, rebuild awareness, and often free up more extra money than you expected in just a week or two.

Click here to get the free No-Spend Challenge Tracker.

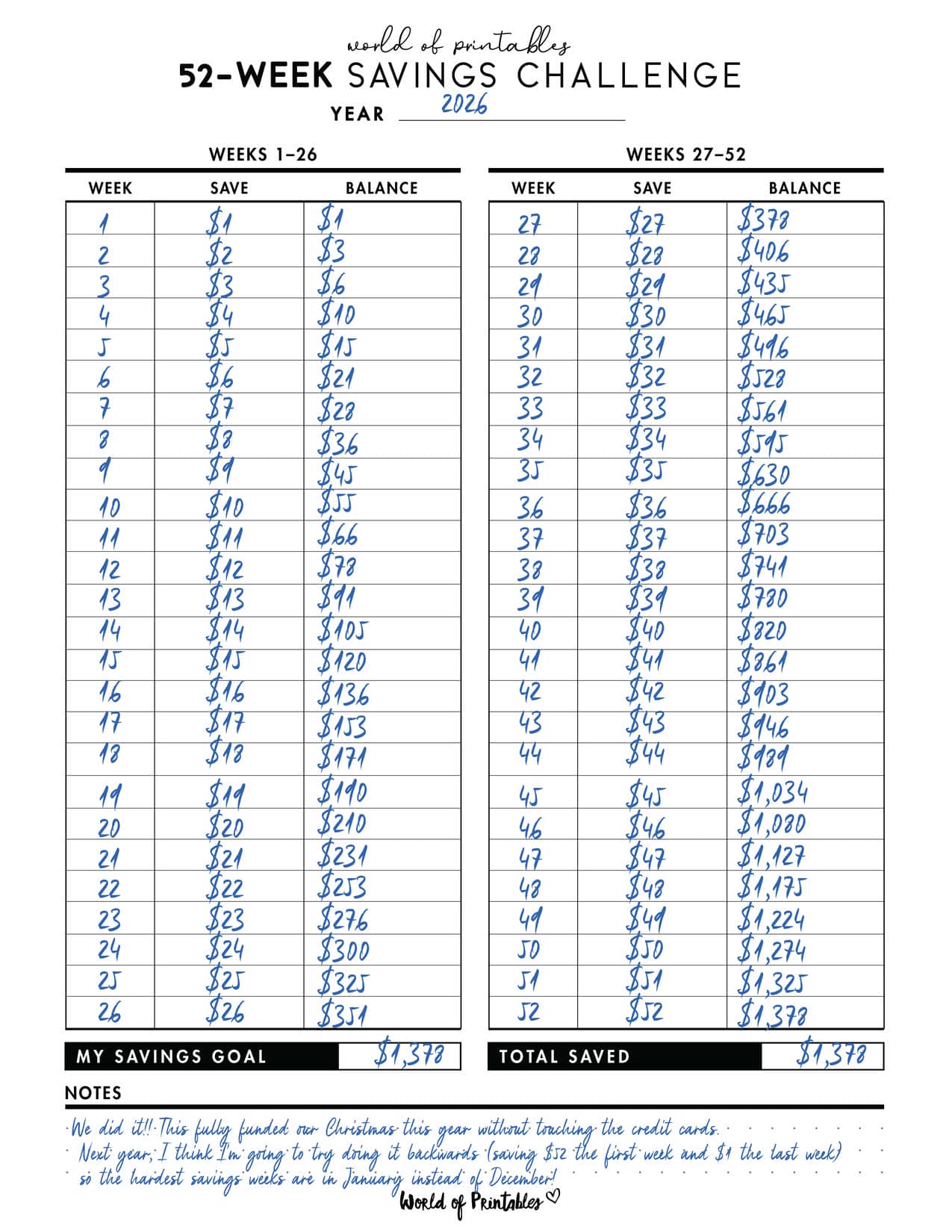

14. 52-Week Savings Challenge

A simple, motivating savings challenge that helps you build money gradually over the course of a year.

The problem:

A big savings goal can feel so overwhelming at the start that it is tempting not to start at all.

What it is:

A simple week-by-week savings challenge where the amount builds gradually over the year.

What it’s really good for:

Making saving feel possible. The early amounts are so small that it is easy to begin, and once the habit is in place, the progress grows almost without you noticing. By the end, those little weekly amounts turn into a surprisingly satisfying savings total.

Click here to get the free 52-Week Savings Challenge.

Phase 6: Auditing and Tax Prep

This section helps you stay organised throughout the year so nothing feels rushed or chaotic later.

15. Online Shopping Tracker

A surprisingly useful page for tracking online orders, deliveries, returns, and refunds so money does not quietly disappear through incomplete purchases or missed refunds.

The problem:

You order several things online, mean to return the ones that did not work out, and then life happens. Before you know it, the return window is gone and your money is gone with it.

What it is:

A simple tracker for online orders, deliveries, returns, and refunds.

What it’s really good for:

Helping you close the loop. This page keeps track of what you ordered, what arrived, what still needs to go back, and when the deadline is. It is incredibly practical and can save you a surprising amount of money over time.

Click here to get the free Online Shopping Tracker.

16. Medical Expense Tracker

Use this to keep healthcare spending, reimbursements, and related records in one place.

The problem:

Medical costs can feel chaotic fast. Bills show up late, insurance adjustments are confusing, and it is hard to remember what you actually paid versus what should have been covered.

What it is:

A central tracker for medical visits, prescriptions, out-of-pocket costs, and reimbursements.

What it’s really good for:

Keeping one of the messiest spending categories organized. When you log your healthcare costs clearly, it becomes much easier to catch billing errors, keep receipts together, and understand what your family is really spending on medical care.

Click here to get the free Medical Expense Tracker.

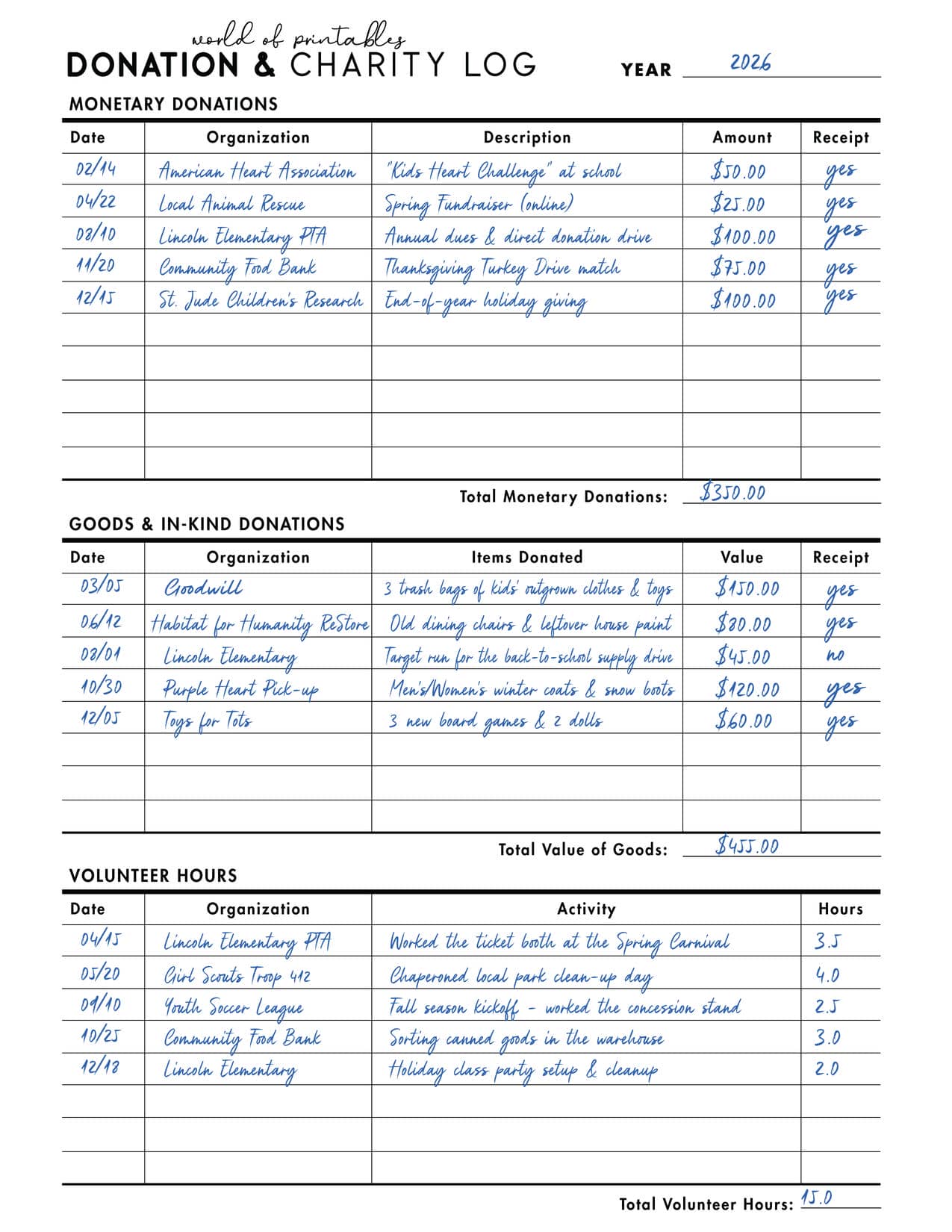

17. Donation and Charity Log

Track your charitable giving and keep your records tidy and easy to review.

The problem:

You donate all year long, but by tax season the receipts are scattered, the dates are fuzzy, and you cannot remember exactly what you gave or when.

What it is:

A year-round tracker for charitable donations, both cash and non-cash.

What it’s really good for:

Helping you keep clear records as you go. Instead of trying to rebuild everything months later, you have one place to log the charity, the date, and the value of each donation. It makes year-end paperwork much easier.

Click here to get the free Donation and Charity Log.

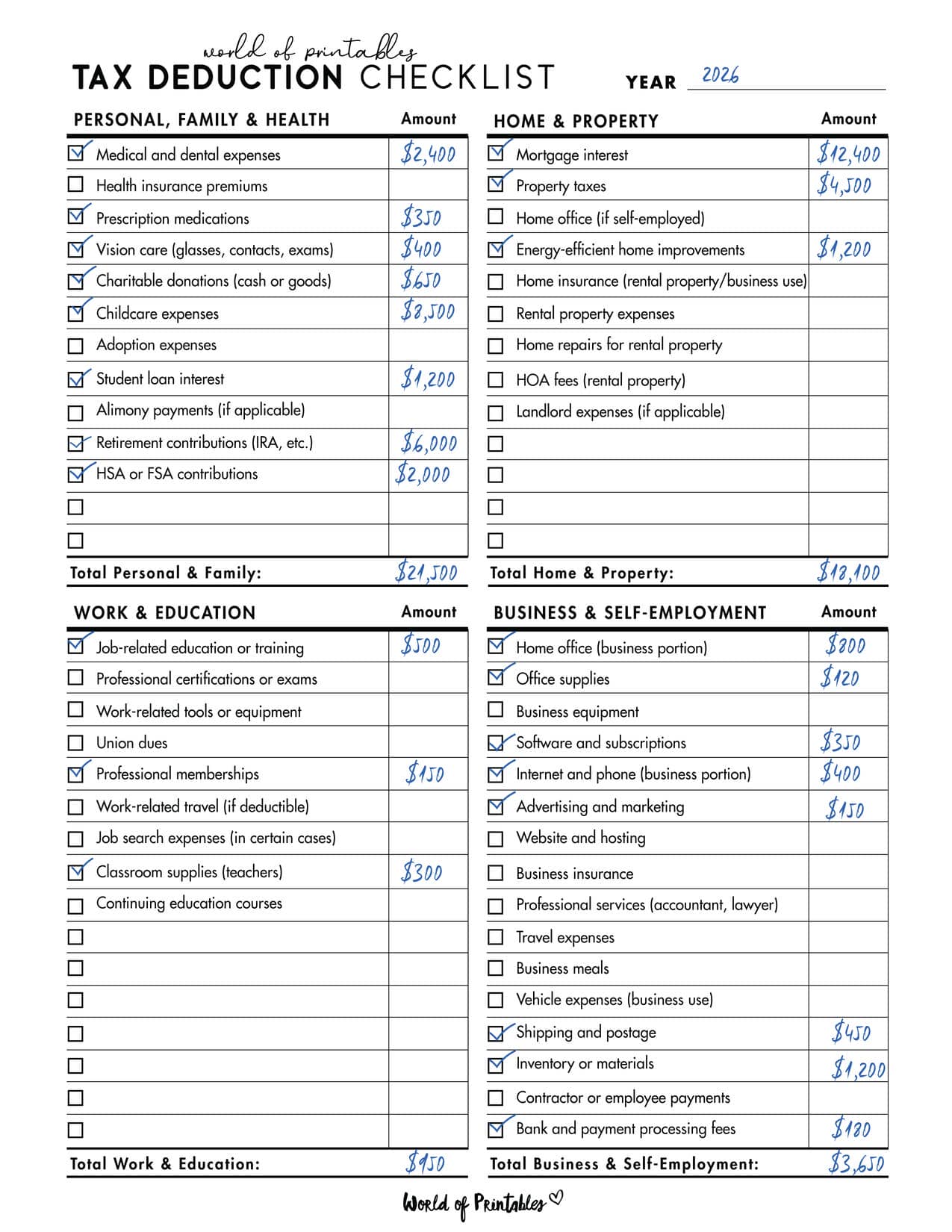

18. Tax Deduction Checklist

A helpful overview page for organising tax-related categories and supporting paperwork.

The problem:

Tax season has a way of making even organized people feel unsure. You sit down to file and suddenly wonder what you forgot to track, what receipts are missing, and whether you overlooked deductions that could have saved you real money.

What it is:

A year-round checklist of common tax-related categories and documents.

What it’s really good for:

Making tax season much less stressful. This page helps you stay aware of what matters throughout the year so you are not scrambling to remember everything at the last minute. It is simple, practical, and very useful for staying organized.

Click here to get the free Tax Deduction Checklist.

Phase 7: Secure Information Hub

This section is for important reference pages that help you keep key financial information organised.

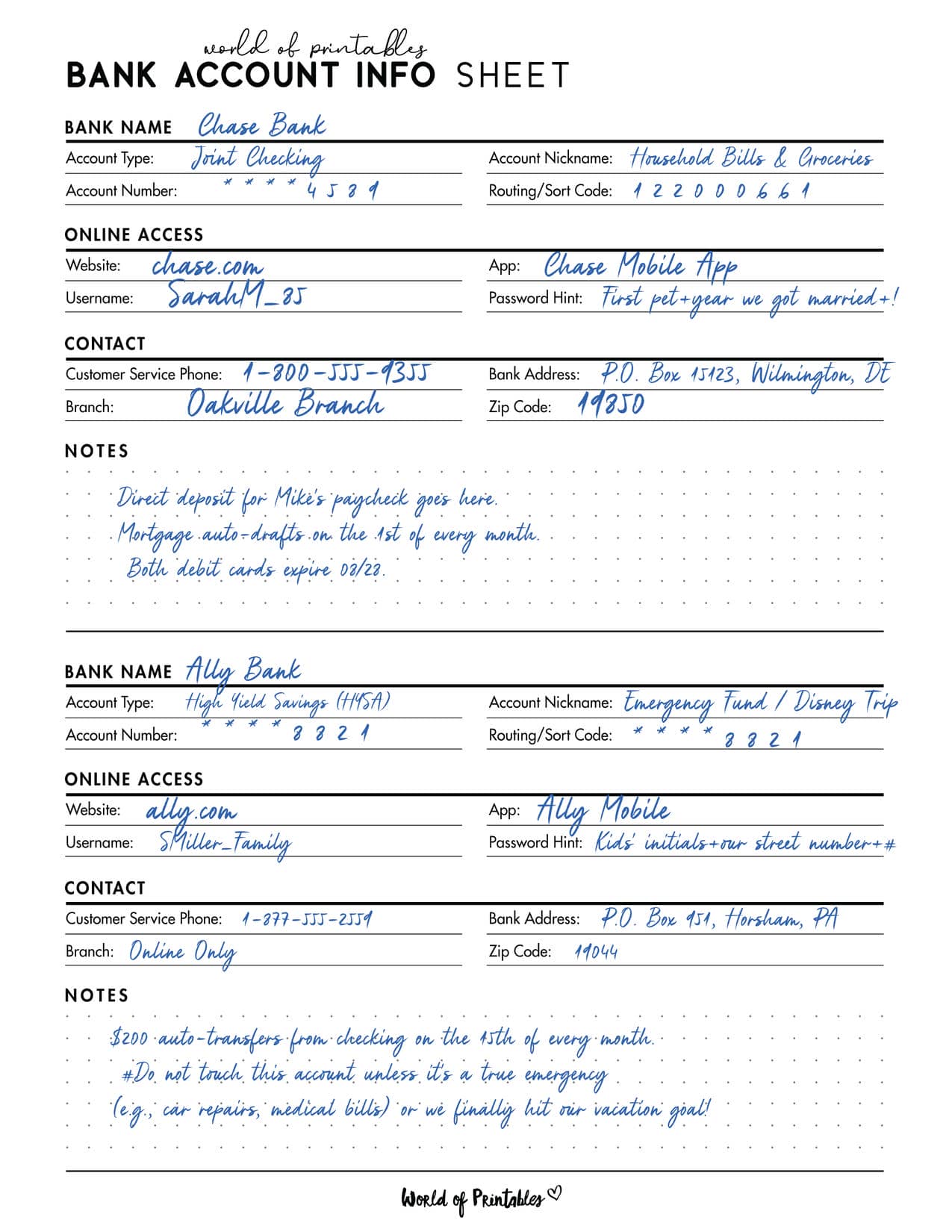

19. Bank Account Info Sheet

A reference page for your bank accounts and essential account details.

The problem:

If your phone is lost, your accounts are locked, or an emergency happens, most families realize very quickly how much important financial information only exists in someone’s head or behind a login.

What it is:

A secure offline reference page for your key bank account details.

What it’s really good for:

Helping your household stay prepared. Stored safely, this page gives you one organized place for important account information that may be needed in a stressful situation. It is not flashy, but it is one of the smartest pages to keep on hand.

Click here to get the free Bank Account Info Sheet.

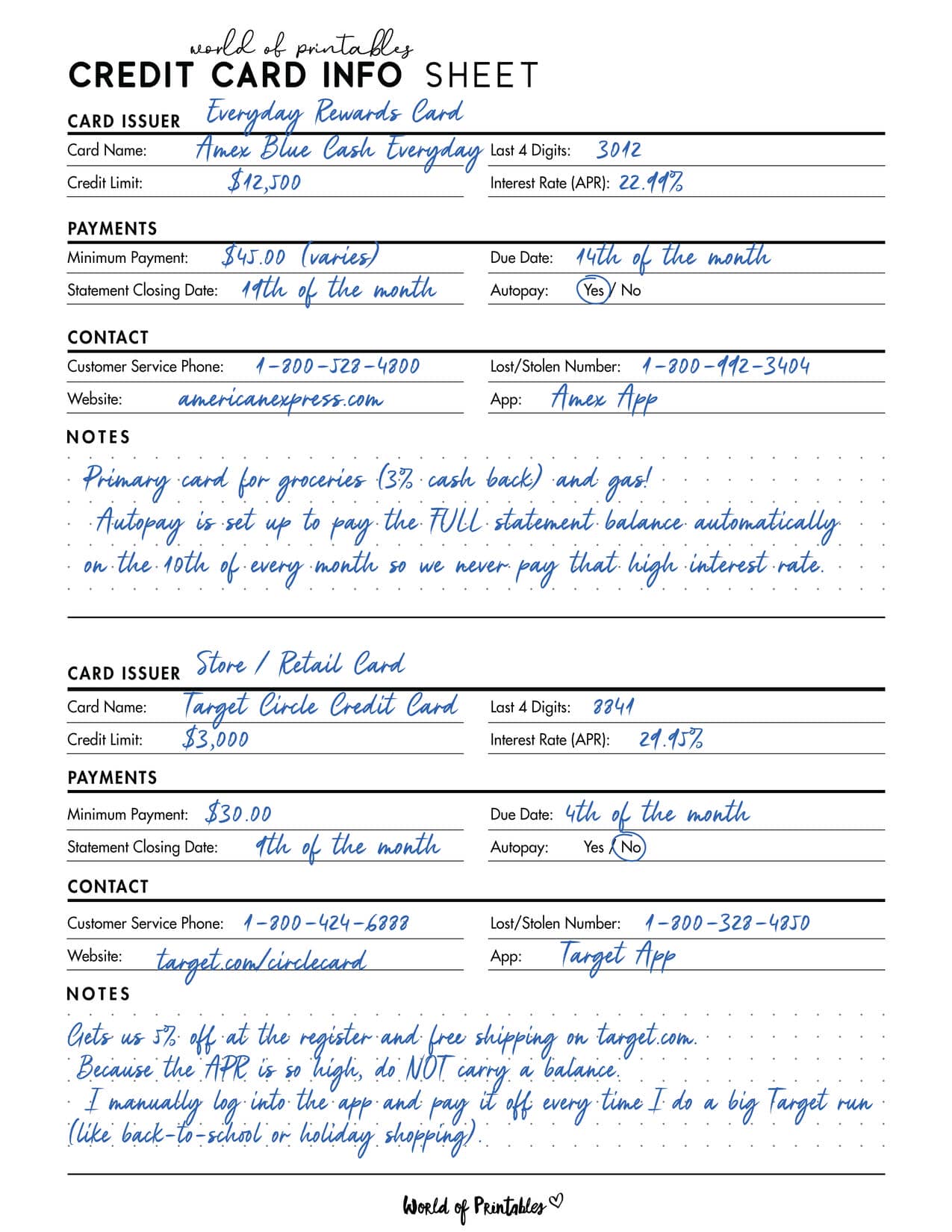

20. Credit Card Info Sheet

A reference page for your credit cards, limits, due dates, and support details.

These pages are especially useful when stored securely at the back of your binder.

The problem:

Losing a wallet is stressful enough. Trying to remember which cards were in it, what the support numbers are, and how to freeze everything quickly only makes it worse.

What it is:

An offline reference page for your credit card details, support numbers, and key account information.

What it’s really good for:

Helping you move fast when it matters. Instead of scrambling to search for numbers or remember account details, you have a clear sheet ready to go. In a stressful moment, that can save both time and money.

Click here to get the free Credit Card Info Sheet.

How to build your Financial Command Binder

This does not need to be complicated.

A strong setup can be very simple.

1) Choose a durable binder

A sturdy D-ring binder works especially well because pages turn more easily and the binder holds up better over time.

2) Use tab dividers

Tabs make a big difference.

You might label them:

- Goals

- Budget

- Bills

- Debt

- Savings

- Tax

- Records

That way, the binder feels like a real system rather than a pile of printables.

3) Print on good paper

If you want the binder to feel more substantial and hold up well, use 28 lb or 32 lb paper instead of standard copy paper.

This is especially helpful for pages you update regularly, like:

- budgets

- spending logs

- trackers

- reference sheets

4) Use page protectors where it makes sense

Great for:

- reference pages

- yearly pages

- secure info sheets

- pages you want to keep clean and intact

5) Start small

Do not try to build the perfect binder in one day.

Start with the pages that solve your most immediate problems:

- budget

- bills

- debt

- savings

Then add more as your system grows.

A simple starter setup if you feel overwhelmed

If you want the easiest possible version to begin with, start with these five pages:

- Monthly Budget Planner

- Bill Payment Calendar

- Daily Spending Log

- Sinking Funds Tracker

- Debt Snowball or Debt Avalanche Tracker

That alone gives you a strong foundation.

Once that feels natural, add:

- annual goals

- net worth

- subscription audit

- emergency fund

- tax pages

- reference pages

Why this kind of system works

A budget binder works because it reduces friction and increases awareness.

Instead of asking:

- What bills are due?

- Where did the money go?

- Which debt should I focus on?

- Did I already budget for that?

- What am I saving for right now?

you can open the binder and see the answer.

That kind of clarity changes how you use your money. It helps you stop reacting and start managing.

And that is the whole point.

Build your binder around your real financial life

The best budget binder is not the most beautiful one or the biggest one.

It is the one that reflects your real life.

If your biggest current stress is debt, build around debt payoff pages.

If your stress is cash flow, start with paycheck planning and a bill calendar.

If your stress is irregular expenses, make sinking funds your priority.

If your stress is tax-time chaos, build the audit and records section first.

This system is modular on purpose. You can make it fit your finances, not force your life into a binder that looks good but never gets used.

Start building your Ultimate Budget Binder

Below is where your full printable library can live, organised by section and linked out to each individual post and printable collection.

Use this page as your master index, your starting point, and your “go back to this” hub whenever you want to add another tool to your system.

Because true financial progress usually does not come from one giant moment.

It comes from having a system that helps you make better decisions over and over again.

AI TRANSPARENCY: Whilst the majority of our creations have been created completely traditionally, occasionally we utilize AI tools in our design process. We acknowledge the advancements in AI technology and leverage them responsibly to optimize our creative output. However, it is important to note that our utilization of AI does not compromise the human element of our work. Our commitment to delivering high-quality designs through a balanced integration of traditional expertise and AI enhancements remains paramount.